Who Is Actually Buying Vineyards?

In today’s market, the majority of institutional vineyard buyers are:

-

Ag-focused private equity funds

-

Funds backed by pension capital

-

University endowments

Family offices were active buyers in prior years, but today many are more often on the seller side.

Attempts at REIT-style vineyard ownership structures in the early 2000s largely proved unsuccessful. Vineyards are operationally complex, biologically sensitive assets. They don’t behave like office buildings or apartment portfolios. The model requires patient capital and hands-on agricultural expertise.

What Institutional Buyers Want (And What They Avoid)

Institutional vineyard buyers are very specific in what they pursue:

What They Want:

-

Producing vineyards

-

Long-term grape contracts

-

Strong water access

-

Scaled production assets

-

Large acreage (the bigger, the better)

They are typically not interested in:

-

Wineries and brands

-

Trophy estates with homes and lifestyle improvements

-

Bare land development (at least not in the current cycle)

-

Distressed properties requiring major replants

There is one vertically integrated player with production facilities, but most institutional buyers focus purely on vineyard assets.

This is farmland as a production platform — not a lifestyle purchase.

Why Vineyards Fit Institutional Portfolios

Vineyards are considered a “permanent crop” investment.

Unlike row crops, which can produce multiple times per year, vineyards require:

-

3–5 years before meaningful production

-

Significant upfront capital

-

No income during establishment

Analysts typically underwrite 30 years of productive life.

That long biological timeline creates:

-

High barriers to entry

-

Capital intensity

-

A need for patient investors

For institutions with long-dated liabilities — pensions and endowments in particular — that timeline aligns well.

Return Expectations and Underwriting

Institutional buyers generally model:

-

8–10%+ average returns

-

Over a 10–30 year hold period

They look at:

-

Blended models (cash flow + land appreciation)

-

IRR, depending on structure

-

Long-term yield stability

Contracts are critical.

Right now, commodity grape pricing is brutal. The numbers simply do not work without strong contracts in place. Contracted fruit dramatically changes underwriting assumptions.

This is not a short-term yield play. It is a long-term asset allocation strategy.

Why the Central Coast Is Attracting Capital

Today, the Central Coast — particularly Paso Robles — is attracting the most institutional interest.

Why?

Scale.

In Napa and Sonoma, high land values make it difficult to pencil deals when you factor in:

-

Farming costs

-

Yield

-

Price per ton

The Central Coast offers larger contiguous acreage and more workable economics.

Vineyard Underwriting Is Not Traditional Private Equity

Buying a company is not the same as buying a vineyard.

Mother Nature is part of the balance sheet.

Institutional vineyard underwriting must account for:

-

Crop risk (mitigated somewhat through insurance)

-

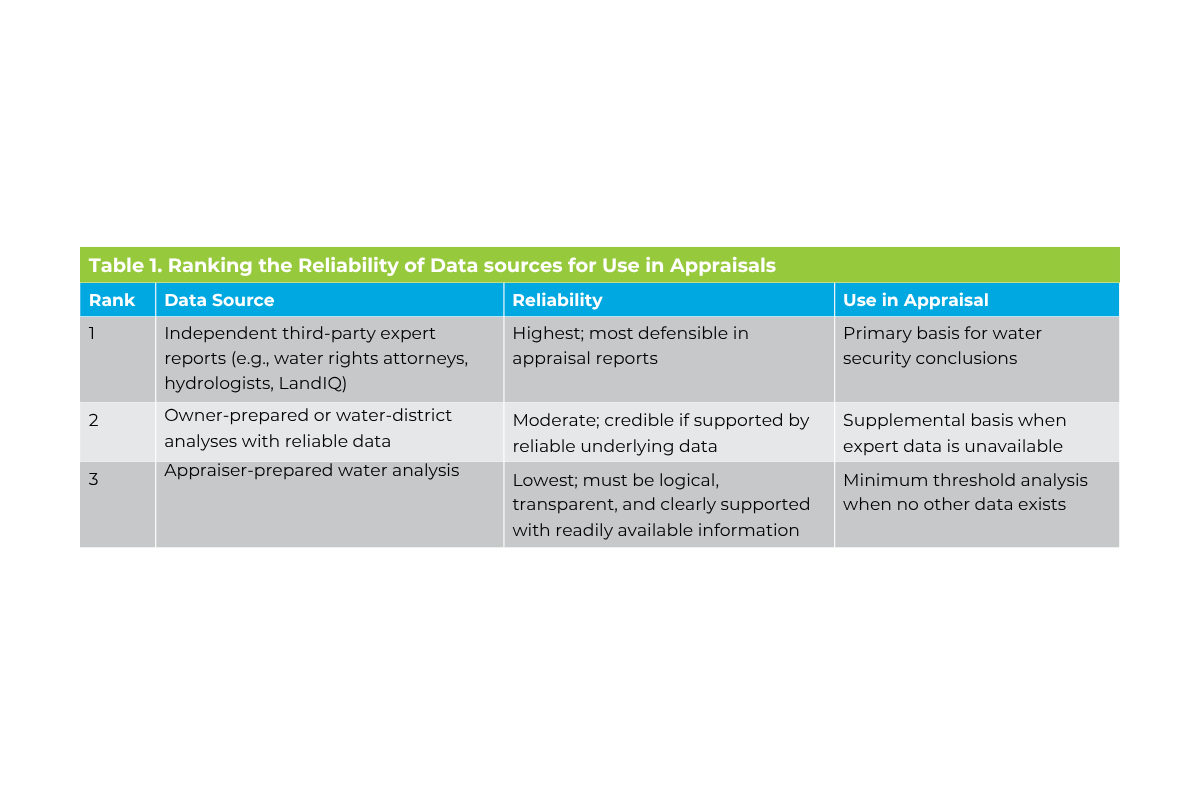

Water security (highly complex and property-specific)

-

Farming management quality

-

Replant cycles (typically 30 years, shorter if disease pressure exists)

-

Grant opportunities that may offset replant costs

-

Mechanization trends

Operational efficiency in vineyards does not look like SG&A cuts in a corporate acquisition. It often comes down to:

-

Capital availability

-

Long-term outlook

-

Local relationships

-

Farming expertise

-

Ability to sell grapes into the right channels

And this is where many out-of-state buyers make mistakes.

The Most Common Institutional Mistake

The biggest mistake I see?

Not partnering with strong local operators.

Vineyards are hyper-local businesses. Water, labor, appellation constraints, yield potential, and buyer relationships all vary dramatically by region.

Without local agricultural relationships, even well-capitalized buyers can struggle.

What Makes a Vineyard “Institutional Quality”?

Not every vineyard qualifies.

Institutional-grade assets typically have:

-

Scale

-

Strong location within recognized appellations

-

Reliable yield history

-

Secure water

-

Existing grape contracts

Structures and lifestyle improvements are usually irrelevant. This is about production performance and long-term asset value.

The Bigger Picture

Private equity fundraising has slowed globally in recent years, but long-term agricultural capital remains interested in permanent crops.

Why?

Because farmland behaves differently than traditional equities and bonds.

And vineyards — when properly structured — offer:

-

Hard asset backing

-

Biological production

-

Inflation hedge characteristics

-

Land appreciation

-

Portfolio diversification

But they require patience. And expertise.

My Perspective From Inside These Deals

Working with wine companies, institutional investors, and bank-owned vineyard assets, I see firsthand how sophisticated capital approaches agricultural real estate.

These investors think in decades.

They focus on water, contracts, yield history, and operational partners.

And the deals that succeed are the ones grounded in real agricultural knowledge — not just financial modeling.

Permanent crops reward discipline and long-term thinking.

They also demand it.

Click here to Join our exclusive market insights newsletter.